Analysis by Tabrez Safarmamadov

Abstract: Increasing demand for critical minerals, lithium, rare earth elements, cobalt, and copper, right now is mainly driven by the global push toward transition to clean energy. This paper explores the growing strategic importance of Central Asian countries in the global critical mineral supply chain. Analyzing the latest statistics, it was discovered that the region is rich in critical minerals that are still not fully exploited. Also, this article covers the interest of leading powers such as China, Russia, the United States, and the European Union in gaining access to these resources. The paper will explore the underlying issues such as landlocked geography, environmental factors, fragile infrastructure, regional cooperation, foreign investment, and value-added mineral processing potential. The paper concludes that with strategic planning, clean development practices, and international cooperation, Central Asia has the potential to be a major contributor to the global clean energy revolution while promoting economic growth and stability in the region.

Keywords: Central Asia, clean energy transition, critical minerals, economic development, geopolitics, infrastructure, international cooperation, investment, mining industry, resource processing

Формирующаяся роль Центральной Азии в глобальной цепочке поставок критически важных минералов

Аннотация: В настоящее время растущий спрос на такие важнейшие минералы, как литий, редкоземельные элементы, кобальт и медь, во многом обусловлен глобальным стремлением к переходу на чистую энергию. В данной работе исследуется возрастающее стратегическое значение стран Центральной Азии в глобальной цепочке поставок критически важных минералов. Анализ последних статистических данных и региональных изменений показывает, что регион обладает богатейшими запасами таких минералов, однако они всё ещё недостаточно освоены. В статье рассматриваются геополитические интересы таких ведущих держав, как Китай, Россия, США и Европейский союз, в получении доступа к этим ресурсам. В работе также анализируются ключевые проблемы, такие как отсутствие выхода к морю, экологические факторы, слабая инфраструктура, региональное сотрудничество, иностранные инвестиции и потенциал развития перерабатывающих производств с добавленной стоимостью. В заключение отмечается, что при наличии стратегического планирования, экологически чистых методов добычи и международного сотрудничества Центральная Азия обладает потенциалом стать одним из основных участников глобальной энергетической трансформации и источником экономического роста и стабильности в регионе.

Ключевые слова: геополитика, горнодобывающая промышленность, инвестиции, инфраструктура, критически важные минералы, международное сотрудничество, переработка ресурсов, переход к чистой энергии, Центральная Азия, экономическое развитие

Introduction

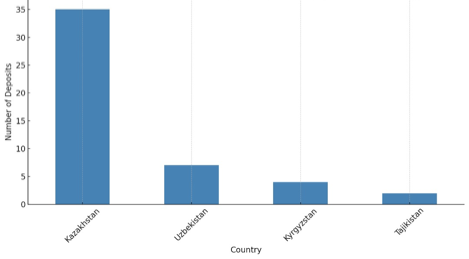

Countries are racing toward decarbonization and clean energy, and critical minerals are emerging as new oil. Lithium, cobalt, rare earth elements (REEs), copper, nickel, graphite are considered critical, because they are valuable materials that can be used to produce solar panels, wind turbines, electric vehicle (EV) batteries, semiconductors, and defense systems. The International Energy Agency has calculated that the world needs to move to four times the amount of production for critical minerals for us to meet the Paris Agreement by 2040, and six times the production for a net-zero outcome by 2050.[1] This extraordinary demand has raised concerns about supply security, since many critical minerals are currently concentrated in a few countries. Central Asian (CA) countries, Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan, are becoming countries of interest, because they have rich mineral resources and opportunities for new partnerships that are outside traditional supply routes. Figure 1 provides a visual overview of the total number of confirmed critical mineral deposits across Central Asia, reflecting the region’s substantial untapped resource potential. This essay explores Central Asia’s growing role in the global critical mineral supply chain. It will not only examine how the region’s resources could reshape energy security, create economic opportunities, and support the fight against climate change, but will highlight the risks that could undermine this potential. To make the argument testable, this paper adds a comparative lens on processing economics including capital expenditures (CAPEX), operating expenses (OPEX) for REE separation, and export route viability (cost/risk for the Middle Corridor versus legacy routes). This makes it possible to assess whether Central Asia’s mineral endowment can translate into bankable projects and deliverable exports.

Figure 1: Number of Critical Mineral Deposits by Country

Source: Central Asia and Caucasus Geoportal; Author’s Illustration[2]

Central Asia’s Critical Mineral Endowment

Central Asia’s five countries together are exceptionally rich in minerals that the global economy needs. In the paper by Roman Vakulchuk and Indra Overland, it is stated that the region holds 38.6% of the world’s manganese ore reserves, 30.07% of chromium, 20% of lead, 12.6% of zinc, 8.7% of titanium, 5.8% of aluminum, 5.3% of copper, and 5.2% of molybdenum.[3] These resources are mainly underdeveloped due to Soviet-era extraction priorities and post-independence economic challenges. However, currently CA is gaining global attention because of high demand for these materials. Additionally, the diversity of the mineral base in Central Asia provides a strong foundation for clean energy and high-tech applications.

A clear reason some states move faster than others is the way policy and investment rules shape risk. In the pages that follow, each country is read through the same lens: how stable the rules are, how state firms and private investors share roles, how offtake and financing are organized, and whether export routes are reliable. Using the same lens makes it easier to explain why Kazakhstan advances while others lag behind.

Kazakhstan is considered to have the largest economy and mining sector in the region. Figure 2 illustrates that Kazakhstan has a large number of potential critical minerals. It is reported to have the region’s largest REE reserves, as well as other strategic metals.[4] The World Bank announced in 2021 that Kazakhstan had been producing 33% of world’s uranium, ranks second in chromium, third for titanium, seventh for zinc, eighth for lead, and eleventh for gold.[5] High extraction and export of uranium position the country as a vital supplier for nations reliant on nuclear energy, including France, China, and Canada. Beyond uranium, Kazakhstan’s copper reserves are equally strategic, and it is a top ten global supplier.[6]

In April 2025, Kazakhstan announced a new REE discovery in Karaganda estimated at 20 million tons, which would make it the third-largest REE deposit globally.[7] However, much of its REE and lithium potential is still undeveloped due to a lack of technology and other capabilities.[8] Rare-earth separation is both expensive to build and costly to run. Limited infrastructure and outdated technology leave most of these minerals untapped. In this regard, President Tokayev has called REEs the country’s “new oil” and prioritized their development.[9] However, success depends upon making wise choices: diversification of economy, infrastructure modernization, and balancing foreign relations. With these challenges resolved, then apart from increasing its own economy, it would play a crucial part in the world’s clean energy transition.

Kazakhstan has moved faster because its policy mix reduces investor uncertainty. Large state champions work alongside private partners under rules that, while imperfect, are predictable enough for long-term contracts. The government has used offtake agreements and export routes that meet buyer requirements, and it has generally kept currency access and repatriation workable for foreign lenders. Together, these features make project finance easier to close and reduce the time from a resource announcement to an operating investment.

Kyrgyzstan’s major mineral resources are more limited in scale but still very important. Figure 2 visualizes this moderate potential clearly. Kyrgyzstan is home to one of the world’s largest gold mines (Kumtor) and copper mines, antimony and coal deposits. Besides gold, Kyrgyzstan also possesses untapped rare earth element (REE) potential, which has very great importance in renewable energy technology and electronics. The Kutessay II mine began operation during Soviet times and resumed afterwards with the help of foreign investors. It has dysprosium and terbium resources, which are minerals used in wind turbines and electric vehicles.[10] Analysts note that Kyrgyzstan has moderate to high potential for nine different critical materials, despite currently modest production.[11] However, its development has been held back by regulatory and social issues.[12] The environmental and social issues in Kyrgyzstan have caused more challenges for mining sector development. There have been several conflicts between the mining companies and locals over land use. The geographical terrain of the country and inadequate transport infrastructure makes mineral exportation from remote mines to global markets costly and labor intensive. Insufficiency of processing facilities forces the country to export raw materials instead of value-added processed goods. Critical minerals in Kyrgyzstan can help in its economic development, but it would require political stability, high-tech infrastructure, and sustainable initiatives to be promoted.

Tajikistan is rich in metals and energy resources. It is home to TALCO, Central Asia’s largest aluminum smelter, and substantial zinc, gold, aluminum, copper, and lead. Tajikistan reportedly ranks among the top 20 countries globally in proven zinc reserves.[13] Its high mountains also contain significant copper and rare metals. Mining these are in process, but Tajikistan’s mountainous landscape and limited infrastructure lead to high mining costs. Tajikistan’s investment pace is shaped by electricity reliability, the weight of enterprises, and the need for long-tenor finance. Currently, projects and agreements from state and international companies are helping to develop these abundant resources, positioning Tajikistan as an emerging hub for mining and industrial expansion in Central Asia.

Turkmenistan’s economy is heavily reliant on oil and gas exports, but it has limited deposits of other minerals such as sulfur, iodine, bromine, potassium salts, and minor metal occurrences. There are not many large-scale mining projects for critical minerals extraction. It is reported that there are more than 150 nonfuel mineral deposits in Turkmenistan.[14] While Turkmenistan is not a big player in the rare metals game right now, it still plays a part in the region’s supply chain. Turkmenistan has a clear policy focus on hydrocarbons and tightly controls who can access data, currency, and contracts. These choices may work for energy, but they make mining projects hard to structure with international lenders. Without greater transparency and investor protections, even viable deposits will move slowly compared with its neighbors.

Uzbekistan is a country rich in gold, copper, and base metals. It is also moving to develop its critical minerals. Figure 2 depicts Uzbekistan’s significant moderate potential across different critical materials. Gold mines in Uzbekistan are some of the largest in the world, and it produces more than 100 tons of gold annually.[15] According to Vakulchuk and Overland, it has 11th largest copper reserve, which are estimated to be around 44 million tons.[16] The government confirmed that there also large reserves of lithium, tungsten, titanium, vanadium and other critical elements. Mining of the critical minerals is not highly developed mainly due to the limited infrastructure. Moreover, gold and uranium mining pose environmental risks, including water pollution and scarcity in a region which already does not have enough water. In 2025, Uzbekistan launched a $2.6 billion minerals initiative covering 76 projects for 28 rare and critical elements, in order to extract these materials with modern technologies and build domestic processing capacity.[17] The stated goals include direct ore processing and increased value-added production. Uzbekistan, as an example, has planned enrichment of tungsten concentrate and other upgrading of raw ores. The country is closing the gap through step-by-step reforms, but many decisions still pass through large state groups. Licensing has become clearer and foreign exchange access is better than a decade ago, yet investors still watch how quickly contracts move and how domestic processing goals are balanced with commercial timelines. The direction of change is positive, which attracts interest, but coordination across agencies and the sequencing of reforms will decide whether projects reach financial close as quickly as in Kazakhstan.

Figure 2. Resource Potential of 22 Critical Materials in Central Asia

Source: Vakulchuk and Overland[18]

The comparison between the CA states suggests that speed of development relies on three factors working together: predictable rules and contracts, bankable sales arrangements that unlock finance, and export routes that buyers trust. Kazakhstan has enough of each to move, Uzbekistan is building them, while Kyrgyzstan, Tajikistan, and Turkmenistan each face a different weak link. Policymakers can therefore target the specific gap, whether it is permitting stability, contract enforcement, financing structures, or corridor reliability, rather than treating ‘investment climate’ as a single, general problem.

Strategic Importance and Geopolitical Interest

Due to uncertainty of the critical mineral supply chain, the Central Asian region attracts the attention of many developed countries. China plays the most active role in CA through its investment programs, mainly through the Belt and Road Initiative (BRI). Most of the investments have been in infrastructure and mining. Cekuta and MacLaren argue in their analysis that huge investments of Chinese and Russian businesses into CA countries can surpass US and EU connections.[19] As Kazakhstan, Kyrgyzstan, and Tajikistan share borders with China, road, pipeline, and rail connections can be established easier rather than with non-neighboring countries. As China controls more than 60% of global rare earth elements (RRE) mining, its access to CA critical minerals makes it more strategically influential in global supply chains.[20]

Another country that is believed to have an interest in Central Asia’s rare earth minerals extraction is Russia. It has strong historical and institutional connections with Central Asia through the Eurasian Economic Union (EAEU) and the Shanghai Cooperation Organization (SCO). There have been many investments from Russia into the energy sector of the CA region. Also, Russia often partners with CA countries and exports some of its mining equipment and expertise. However, the recent sanctions that the Russian economy faces has limited new investments in the energy sector of the CA region. Many experts believe that Russia acts as a counterweight to China, which causes Central Asian governments to carefully think before making partnership decisions with the two in order to avoid becoming too dependent on either of them. The SCO includes all the Central Asian states, China and Russia and provides opportunity for regional cooperation, security coordination, and economic development.[21]

Involvement of the United States in Central Asian minerals has only recently started. The C5+1, which involves five Central Asian countries and the US, focuses on integrating the materials of CA countries into the western supply chains. In 2023, leaders of these nations launched the Critical Minerals Dialogue (CMD), which focuses on the involvement of minerals from CA to global mineral supply chains, promoting the clean energy transition, and strengthening regional cooperation.[22] There have been several visits by US officials to Kazakhstan and Uzbekistan to discuss joint exploration and processing projects. Experts believe that one of the main reasons is that Washington views Central Asia as a way to help reduce American and European dependence on Chinese minerals. The US has offered funding and its expertise through USAID, EXIM, and the Development Finance Corporation in order to connect US companies with CA mining projects. Moreover, in 2023, the US organized the Minerals Security Partnership dialogue and invited CA states to join the global effort aimed at securing sustainable and resilient critical mineral supply chains.[23]

Similar to other major global actors, the European Union also started engaging in relationships with Central Asian states. In 2025, in Uzbekistan, the first Summit of EU and Central Asian leaders was held, where regional stability, sustainable energy cooperation, trade facilitation, and enhanced transport connectivity were discussed.[24]

In order to tighten the relationship with Central Asian countries, the EU has pledged to invest more than €2.5 billion as part of its Global Gateway program. The investment will mostly enhance the mining and processing infrastructure in the region.[25] Moreover, there have been several other agreements between Central Asian countries, including a key partnership between the EU and Kazakhstan for collaboration on the extraction of raw minerals and processing, focusing on renewable energy and circular economy practices.[26] Alongside the 2022 EU-Kazakhstan Memorandum of Understanding (MoU), Uzbekistan also signed a strategic MoU with the EU, anchoring Central Asia in the EU’s Critical Raw Materials diversification push.[27] Similar to other developed countries, the strategy of the EU is to strengthen its supply chains for critical raw materials and reduce dependency on single-source suppliers. It can be said that the EU’s involvement in Central Asia is driven by both economic necessity and geopolitical competition. Success depends on the balance between its sustainable development agenda and the political realities of the region.

Central Asia’s main strength in today’s economy is reliable delivery, even if the price is slightly higher. Many buyers will pay a bit more if shipments arrive when promised and contracts are clear and stable. As border and port delays shrink and permits move faster, the region’s risk mark-up falls, so total costs move closer to rivals. That dependability leads to more long-term purchase deals, which in turn leads to more financing. Countries can improve logistics and processing with better financing, which leads to lower costs and stronger trust.

Challenges to Development

Even though many of the region’s critical minerals are confirmed, there are still many other obstacles that prevent Central Asia from becoming a stable global supplier. The first and most significant obstacle is its geographical location, as the region is mostly landlocked, limiting the building of rail lines and highways. Many mineral deposits lie in remote mountains or deserts far from export routes. Figure 3 maps out how dispersed and remote many of these deposits are, especially in southern Tajikistan and Kyrgyzstan. In order to export the heavy ores from many Central Asian countries, it will require transit through neighboring countries or the Caspian Sea to reach the global market. There are several projects under development that aim to connect western countries with the CA region. One of them is the Trans Caspian ‘Middle Corridor’, through Azerbaijan and Georgia to Europe.[28] This corridor would provide an opportunity for faster and easier access to the global market for the CA region.

Map 1. Rare Earth Elements and Rare Metal Inventory in Central Asia

Source: U.S. Geological Survey[29]

Another major barrier for extraction of critical minerals and REE are the environmental and social concerns. Mining requires a large amount of water and energy, which will decrease the availability of them for the population, animals and agriculture. Local communities are often suspicious of foreign mining firms because of past environmental damage. Mining companies should understand that it is important to make full environmental assessments and probably invest more revenues in the local economy. Also, in order to secure both its ecological integrity and its role as a main player in the global critical mineral supply chain, it is essential that all countries operating in CA implement good environmental regulations, invest in sustainable mining technologies, and promote transparent governance practices.

Opportunities and Path Forward

Critical minerals provide a unique opportunity for Central Asian countries to convert the region into an economic powerhouse by fostering local industrial development. Observers note that “rare earths can be the engine of economic growth in Central Asia,” given their key role in green technology and defense.[30] To take advantage of this opportunity, nations need to come up with an efficient plan that matches their economic goals with the realities of geopolitics.

Regional cooperation among the five Central Asian countries can bring economic and developmental benefits for all of them. Presently, the states are involved in a variety of different negotiations of cooperation. Critical mineral importance makes these connections easier, such as the “C5+1” framework and other dialogues (C5+GCC, C5+Japan). Export routes change the final price and the risk for buyers. The old route through Russia may be cheaper but now faces sanctions and contract risk. There are already Trans-Caspian “Middle Corridor” rail and port links across the Caspian Sea, which currently move some Kazakh uranium to Europe.[31] It still has bottlenecks at ports and rail transfers, which can slow trains and raise costs. Even so, some buyers will pay a small premium for a route that avoids Russia and offers clearer policy support. Also, Sanchez and his colleagues argue that utilizing such routes allows producers to bypass Russian territory, which makes the material prized by Western buyers.[32] Creation of joint institutions and research would allow for new studies and efficient mining. At the same time, it will make the region transparent to investors, academia, and regulators. Having common interests will improve cooperation within the region and can lead to more multinational funding for joint investments in infrastructure or the energy sector.

Moreover, the high reserves of critical resources attract new investment opportunities into the Central Asian region. International investors are interested in new mineral sources, and Central Asia can attract FDI by offering clear incentives such as stable taxes or equity partnerships to the investors. Also, financial mechanisms can be created in the region. For example, CA countries can agree to a Central Asian REE Reserve Fund, and this strategic reserve and credit mechanism could help to stabilize price fluctuations and support the development of new projects. Central Asian countries should diversify their investors base. Sanchez notes that even though there already some agreements with the US, EU, India, Japan and South Korea, the Central Asian government should look for cooperation with other regions such as the Middle East and the global South.[33] Getting investment from a broad set of countries will strengthen local sovereignty and will integrate the region into multiple supply chains.

Critical minerals also provide opportunities for the Central Asian countries to start manufacturing value added products rather than just exporting raw ore. Policymakers and investors point out that building local processing plants will bring more economic benefits compared to direct export of raw ore. The agreements between the investors and local government should focus on such value-added projects. Kyrgyzstan recently made an announcement that it plans to commission a rare-earth processing plant at the Kutessay-II mine.[34] As global experts advise, the region’s long-term success depends on shifting toward value-added processing which brings more economic benefits.

Conclusion

Central Asia’s vast mineral reserves makes it a region of emerging importance in the global critical minerals supply chain but realizing that potential depends on difficult policy choices. Governments need to figure out how to protect the environment and at the same time allow quick extraction.

Also, the question of how to attract foreign investment without losing control of important resources remains unanswered. Many major powers already seek partnership with Central Asian countries through different initiatives. In the long run, if Central Asia can overcome infrastructure, regulatory, and environmental challenges, it could indeed become a ‘new hotspot’ and major global supplier of critical materials. This will also be an influence on regional stability and long-term national sovereignty. Faster mining and extraction of REE might make quick money, but in the absence of proper regulation, ruin ecosystems. A more sustainable, slower process with smart policies and international collaboration can protect communities and lead to cleaner growth.

In the coming decade, Central Asian leaders will need to set clear priorities such as: will they focus on short-term export earnings or invest in domestic processing and green technologies? Will they pursue inclusive growth or rely on state-centered control? The choices made today will impact the future of the region in becoming just a source of raw materials or emerge as a sustainable and strategic partner in the global clean energy future.

About Tabrez Safarmamadov

Tabrez Safarmamadov is anMA student in Economic Governance and Development Programme at the OSCE Academy in Bishkek. He graduated with a BA in Global Economics from University of Central Asia and specializes in research on development problems such as economic inequality, institutional change, and policy effectiveness in developing economies. His research interests also include sustainable development, governance in the Central Asian region, and international economic cooperation. Well-versed in policy analysis and quantitative analysis, Tabrez continues to be dedicated to evidence-based development strategies and inclusive economic policy-making in the region and globally.

Address for correspondence:

tabrez.safarmamad@gmail.com

[1] International Energy Agency, The Role of Critical Minerals in Clean Energy Transitions, World Energy Outlook Special Report, May 2021, https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions.

[2] CAC GeoPortal, “Critical Mineral Resources in Central Asia and Caucasus Region,” accessed May 28, 2025, https://www.cacgeoportal.com/datasets/cacgeoportal-hub::critical-mineral-resources-in-central-asia-and-caucasus-region/about.

[3] Roman Vakulchuk and Indra Overland, “Central Asia is a Missing Link in Analyses of Critical Materials,” One Earth 4, no. 12 (December 17, 2021): 1678–90, https://doi.org/10.1016/j.oneear.2021.11.012.

[4] Wilder Alejandro Sanchez, Ariel Cohen, and Wesley Alexander Hill, Leveraging Central Asia’s Rare Earth Elements for Economic Growth, IMA Strategy, December 2023, https://imastrategy.com/leveraging-central-asias-rare-earth-elements-for-economic-growth/.

[5] World Bank, Mining Sector Diagnostic: Kazakhstan, February 2023, https://documents1.worldbank.org/curated/en/099081823001539573/pdf/P17674501063760b08b290a4ae6547845d.pdf.

[6] Ibid.

[7] CCASC. “1st EU-Central Asia Summit Takes Place in Samarkand; Kazakhstan Discovers 20 Mln. Ton of Rare Earth Metal Deposits,” April 7, 2025. https://www.chinacentralasia.org/projects/media-monitoring-reports/306-media-monitoring-07-04-2025.

[8] Ron MacLaren, Robert F. Cekuta, and Dante Schulz, Sourcing Rare Earth Minerals in Central Asia, Caspian Policy Center Policy Brief, June 2022, https://api.caspianpolicy.org/media/ckeditor_media/2022/06/15/sourcing-rare-earth-minerals-in-central-asia_lUGwsVB.pdf.

[9] “US Looks to Draw Central Asia into Critical Minerals Supply Chains,” MineralPrices.com, March 18, 2024, https://mineralprices.com/us-looks-to-draw-central-asia-into-critical-minerals-supply-chains/.

[10] Karine M. Renaud, “The Mineral Industry of Kyrgyzstan,” in 2016 Minerals Yearbook, Volume III, Area Reports: International—Europe and Central Eurasia, U.S. Geological Survey, November 2021, https://pubs.usgs.gov/myb/vol3/2016/myb3-2016-kyrgyzstan.pdf.

[11] Roman Vakulchuk and Indra Overland, “Central Asia is a Missing Link in Analyses of Critical Materials”.

[12] Ron MacLaren, Robert F. Cekuta, and Dante Schulz, Sourcing Rare Earth Minerals in Central Asia.

[13] “Central Asia is a Missing Link in Analyses of Critical Materials”.

[14] Asian Development Bank, “Mineral Resources: Geologists’ Paradise,” In Central Asia Atlas of Natural Resources (Manila: Asian Development Bank, 2010): 62–67, https://www.carecprogram.org/uploads/Mineral-Resources-Geologists-Paradise.pdf.

[15] Elena Safirova, “The Mineral Industry of Uzbekistan,” in Minerals Yearbook, Volume III, Area Reports: International—Europe and Central Eurasia, U.S. Geological Survey, June 2023, https://pubs.usgs.gov/myb/vol3/2020-21/myb3-2020-21-uzbekistan.pdf.

[16] “Central Asia is a Missing Link in Analyses of Critical Materials”.

[17] “Uzbekistan Launches Drive to Develop Minerals & Mining Sector,” Eurasianet, March 10, 2025, https://eurasianet.org/uzbekistan-launches-drive-to-develop-minerals-mining-sector.

[18] “Central Asia is a Missing Link in Analyses of Critical Materials”.

[19] Sourcing Rare Earth Minerals in Central Asia.

[20] “US Looks to Draw Central Asia into Critical Minerals Supply Chains,” MineralPrices.com.

[21] “Shanghai Cooperation Organization Is Playing an Important Role in Ensuring Regional Security and Stability,” The Shanghai Cooperation Organisation, January 25, 2024, https://eng.sectsco.org/20240125/1244550.html.

[22] “US Looks to Draw Central Asia Into Critical Minerals Supply Chains”.

[23] Ibid.

[24] “First EU-Central Asia Summit,” Consilium, April 4, 2025, https://www.consilium.europa.eu/en/meetings/international-summit/2025/04/04/.

[25] “Rethinking EU Strategy in Central Asia,” DGAP, December 18, 2024, https://dgap.org/en/research/publications/rethinking-eu-strategy-central-asia.

[26] European Commission, Memorandum of Understanding between…, 2022, https://single-market-economy.ec.europa.eu/system/files/2022-11/EU-KAZ-MoU-signed_en.pdf.

[27] Otabek Akromov, “From Margins to the Core: The Rise of Central Asia in the Race for Critical Minerals?” The Hague Research Institute, October 2025, https://hagueresearch.org/from-margins-to-the-core-the-rise-of-central-asia-in-the-race-for-critical-minerals/.

[28] Eric Rudenshiold, “The Trans-Caspian Middle Corridor Is Thriving,” Central Asia Program, April 2024, https://centralasiaprogram.org/publications-all/the-trans-caspian-middle-corridor-is-thriving/.

[29] Susan J. Hall, Ryan D. Taylor, and Mark D. Mihalasky, “Rare Earth Element and Rare Metal Inventory of Central Asia,” U.S. Geological Survey Fact Sheet 2017–3089, March 2018, https://pubs.usgs.gov/fs/2017/3089/fs20173089.pdf.

[30] Aruzhan Ualikhanova, “US Experts Research Central Asia’s Potential in Rare Earths, Call for Global Supply Chain Diversification,” The Astana Times, January 27, 2024, https://astanatimes.com/2024/01/us-experts-research-central-asias-potential-in-rare-earths-call-for-global-supply-chain-diversification/.

[31] Wilder Alejandro Sanchez, Ariel Cohen, and Wesley Alexander Hill, Leveraging Central Asia’s Rare Earth Elements for Economic Growth, International Tax and Investment Center, December 2023, https://static1.squarespace.com/static/5a789b2a1f318da5a590af4a/t/65792cb79087211182910e96/1702440120367/Leveraging+Central+Asia%E2%80%99s+Rare+Earth+Elements+for+Economic+Growth.pdf.

[32] Wilder Alejandro Sanchez, Ariel Cohen, and Wesley Alexander Hill, Leveraging Central Asia’s Rare Elements for Economic Growth.

[33] Ibid.

[34] Ibid.